India's Payment Infra

2025 Mar 30

See all posts

India's Payment Infra

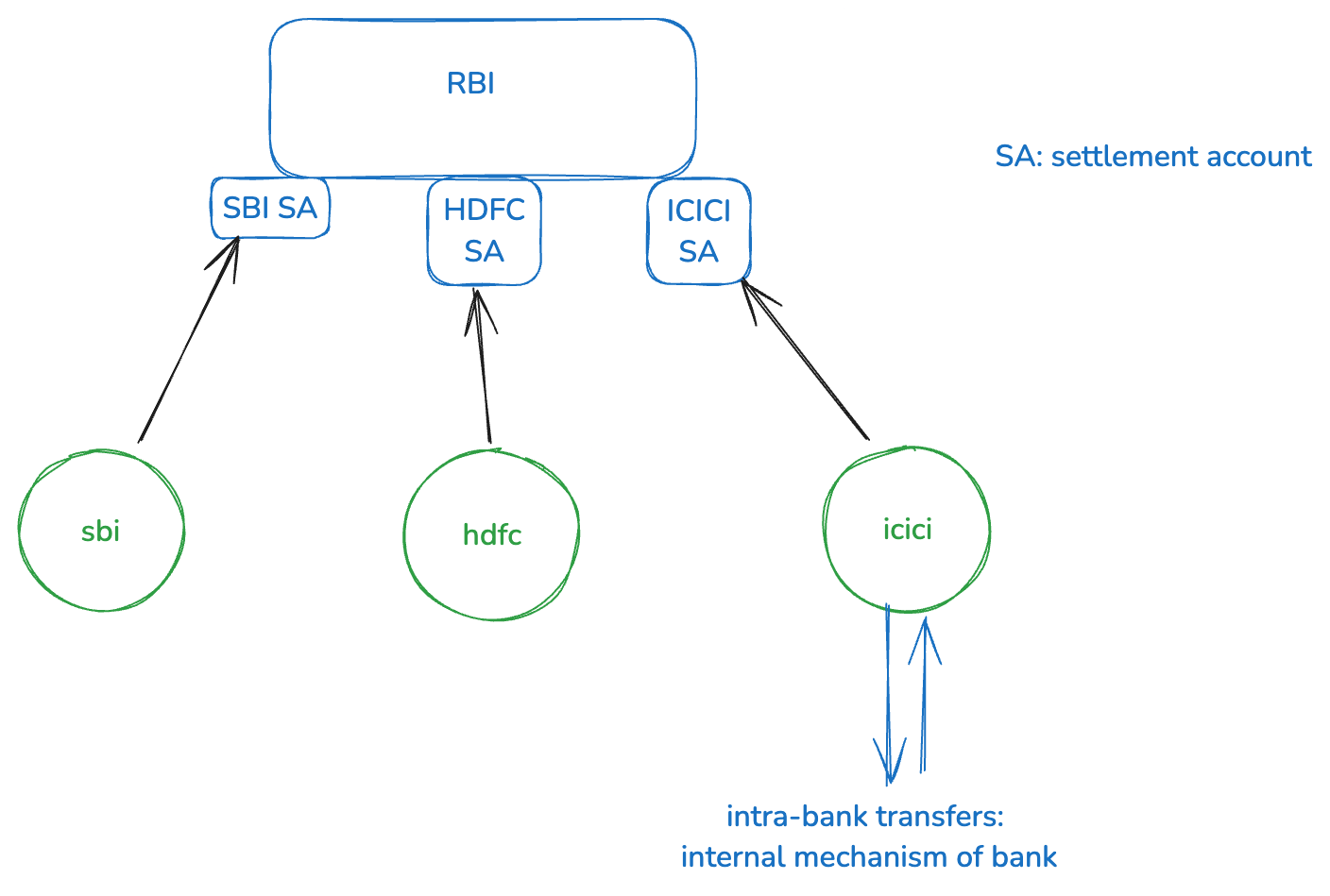

RBI: bank of banks

RBI: bank of banks

- intra bank payments are easy-peasy, just update some numbers within the bank's systems.

- for inter-bank payments, the settlement layer is provided by RBI. Each bank has a settlement account with the RBI (the bank of banks)

- RBI provides RTGS, which does large transfers immediately (i.e. the interbank settlement done) and irrevocably. The fees is consequently high due to this guarantee.

- RBI also provides NEFT, wherein the settlement happens in periodic batches (so it might take a few hours before the transfer is executed).

- NPCI (national payments corporation of india) is a NPO started by RBI to research on payment infra. They came up with IMPS.

- IMPS has a interbank messaging layer, which allows the recipient's account to immediately reflect the credit. In the background though, RBI will do the IMPS settlements in batches (similar, but more frequent than NEFT). NPCI provides the messaging infra (central switching and message routing system).

- UPI is similar to IMPS, in that it uses messaging layer + RBI's settlement layer. But it has a different architecture. The messaging layer for example is mobile-first and API-based architecture, allowing a more comprehensive network of apps/fintech/banks/vendors etc. to participate in the payment network. Also, they have more friendly UX (QR code, upi id, phone number) for a smartphone heavy country.

Other countries which have slower real-time payment systems, typically don't have fast protocols like UPI or IMPS. There can be multiple reasons for that including - The RBI-equivalent body there didn't push for these innovations + regulatory approach, difficulties in standardising due to factors like different technical capabilities.

It was interesting to see the local payment infra. There are many missing things from here - international transfers (SWIFT etc.), debit/credit cards, and the new boom in stablecoins.

India's Payment Infra

2025 Mar 30 See all postsOther countries which have slower real-time payment systems, typically don't have fast protocols like UPI or IMPS. There can be multiple reasons for that including - The RBI-equivalent body there didn't push for these innovations + regulatory approach, difficulties in standardising due to factors like different technical capabilities.

It was interesting to see the local payment infra. There are many missing things from here - international transfers (SWIFT etc.), debit/credit cards, and the new boom in stablecoins.